The Essential Tax Guide For Sri Lankan Expats in 2026: Residency and Remittance

The Essential Tax Guide For Sri Lankan Expats in 2026: Residency and Remittance

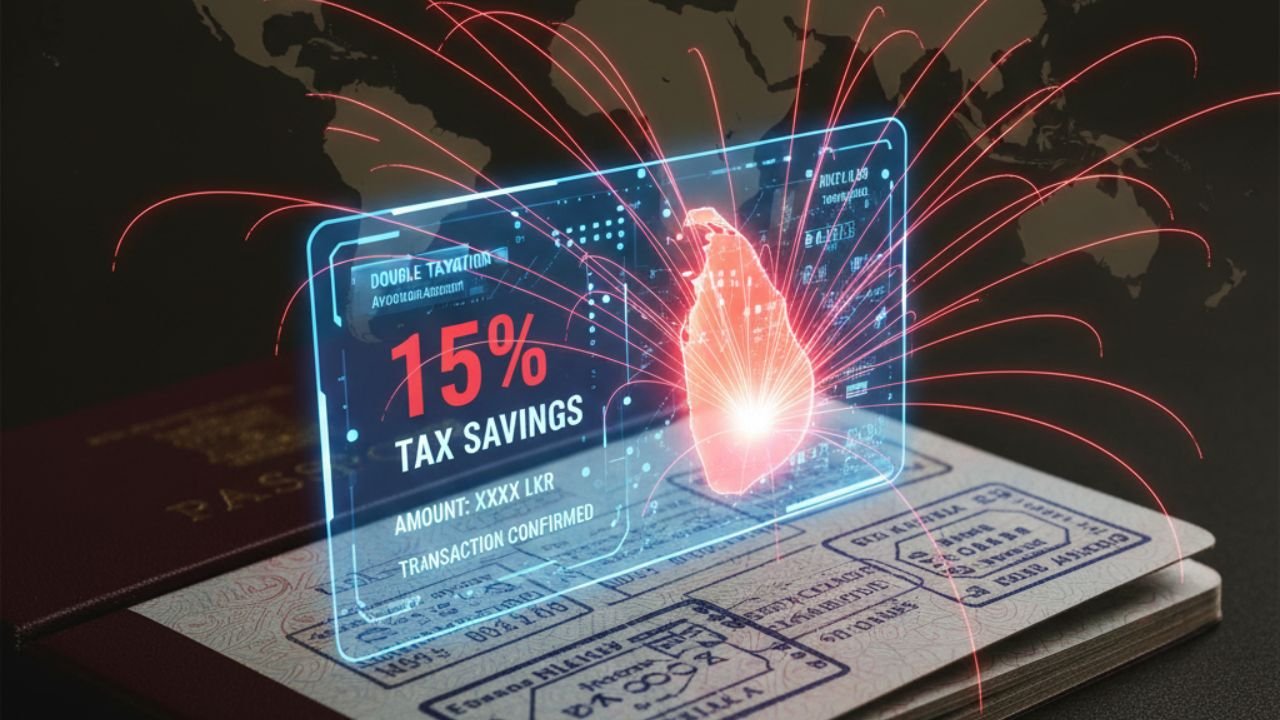

Tax guide for sri lankan expats in 2026 has become the single most critical piece of financial literature for the global diaspora. Following the economic restructuring and the introduction of new fiscal policies by the Inland Revenue Department (IRD), the landscape for overseas earnings, investments, and remittances has fundamentally changed. The key pivot lies in the strict enforcement of residency rules and the introduction of a new 15% tax on foreign-sourced income remitted to Sri Lanka (Source 1.3, 3.4).

This comprehensive 2000–2500 word blueprint serves as the essential strategic companion for every global Lankan, whether you are a high-earning freelancer remitting funds, an investor managing assets in Colombo, or a permanent migrant worker. We will dissect the three crucial pillars of expat taxation: Tax Residency, the implications of the Remittance Tax, and the indispensable strategies for utilizing Double Taxation Avoidance Agreements (DTAAs) and Foreign Tax Credits (FTC) to ensure compliance while legally preserving your global wealth. Strategic planning is no longer optional; it is essential to navigate this new financial era successfully.

Part I: The Foundation: Determining Tax Residency

Your entire tax obligation is governed by one fundamental status: Are you a tax resident of Sri Lanka, a non-resident, or subject to dual residency? Understanding this is the crucial first step for every Sri Lankan abroad.

1. The 183-Day Rule (Physical Presence Test)

Sri Lanka’s primary criterion for determining tax residency for individuals remains the physical presence test, often known as the 183-day rule (Source 2.2, 3.3).

-

Tax Resident: An individual is generally considered a tax resident for a given year of assessment (April 1 to March 31) if they are present in Sri Lanka for a period or periods amounting to 183 days or more during that year (Source 2.2).

-

Implication: A resident is subject to tax on their worldwide income (Source 2.1). This includes income derived from employment, business, and investments both within Sri Lanka and abroad.

-

-

Non-Resident: A non-resident individual is only charged tax on income that has a source in Sri Lanka (Source 2.1).

Crucial Tip for Expats: Meticulous documentation of your physical whereabouts (passport stamps, travel records, utility bills) is now critical, especially if you spend time in Sri Lanka for family or business (Source 2.2). Failing to prove non-residency can expose your entire global income to Sri Lankan taxation.

2. The Citizen Loophole and Relief

A Sri Lankan citizen who is a non-resident is still subject to tax on income arising or derived from Sri Lanka (Source 2.1). However, all individuals, including citizens (whether resident or non-resident), are entitled to the personal tax-free allowance, which is currently set at LKR 1,800,000 per year (effective from April 1, 2025) (Source 2.1).

Part II: The New 15% Remittance Tax and Compliance

The most significant change for individuals and service exporters (freelancers, consultants, IT professionals) who choose to bring their foreign earnings back home is the new flat tax.

1. The 15% Tax on Foreign-Sourced Income

Effective from April 1, 2025, foreign-sourced income earned in foreign currency and remitted to Sri Lanka through a licensed bank will be taxed at a flat rate of 15% (Source 1.1, 1.3, 3.4).

-

Who is Affected? This primarily impacts the growing segment of high-earning individuals (IT, BPO, KPO, freelancers) and companies that provide services to overseas clients and are paid in foreign currency (Source 1.3).

-

The Incentive: The key distinction is the method of remittance.

-

Remitted via Bank: The income is subject to the lower, flat 15% tax, which acts as a final tax (Source 3.4).

-

Not Remitted via Bank (Kept Offshore or Brought in via Informal Channels): This income will be subject to the standard, much higher progressive tax rates, which for the highest earners can reach up to 36% (Source 3.4, 3.3).

-

2. The Role of the Banking System (Send Money Pillar)

The banking system has become the tax compliance mechanism. For the diaspora utilizing platforms like Wise or Revolut for international money transfer (Internal Link: Link to your Send Money article), ensuring the funds arrive in your Sri Lankan bank account and are correctly declared as foreign service income is paramount to securing the lower 15% rate (Source 3.4).

3. Tax Filing Deadlines

Regardless of where you are in the world, compliance is mandatory if you have taxable income in Sri Lanka.

-

Estimated Tax Statement (SET): Due on or before August 15th of the current year of assessment (Source 2.1).

-

Income Tax Return (IT Return): Due on or before November 30th of the next succeeding year of assessment (Source 2.1).

Part III: Avoiding Double Taxation: DTAAs and FTCs

The most common fear for the global Lankan is being taxed on the same income twice—once in the country of residence (e.g., UK, Australia) and once in Sri Lanka. This is prevented through bilateral agreements and unilateral tax credits.

1. Double Taxation Avoidance Agreements (DTAAs)

Sri Lanka has DTAAs with numerous countries globally (Source 1.2, 3.3).

-

Purpose: DTAAs are treaties that override domestic law, setting clear rules on which country has the primary right to tax specific types of income (e.g., employment, pensions, dividends, rental income) to prevent or reduce double taxation.

-

Access Requirement: To benefit from a DTAA, you typically must obtain a Tax Residency Certificate (TRC) from the country where you are claiming residency (Source 2.2).

-

Tie-Breaker Rules: If you meet the residency criteria in two countries (a common Nomad Life issue), the DTAA tie-breaker rules (e.g., where is your permanent home, where is your center of vital interests) determine the final tax home (Source 2.2).

2. The Foreign Tax Credit (FTC) Strategy

Even where a DTAA does not apply or does not fully cover the income, Sri Lanka provides a unilateral relief mechanism (Source 3.4, 3.5).

-

Mechanism: If you have paid tax on your foreign income in the country where it was earned, you can claim an FTC against your Sri Lankan tax liability.

-

The 15% Minimum Rule: Crucially, for the foreign income remitted to Sri Lanka, the Inland Revenue Act mandates that if the tax paid overseas is less than the 15% rate, you must pay the difference to the IRD (Source 1.5). If you paid more than 15% abroad, you are usually exempt from further tax in Sri Lanka on that remitted income, but the credit cannot be carried forward or refunded (Source 3.5).

Part IV: Strategic Expat Tax Planning and Advisory

The complexity of the 2026 tax landscape makes professional advice non-negotiable for high-net-worth individuals, property owners, and digital nomads.

1. Investment Asset Realization (Banking & Finance Pillar)

Gains from the realization of investment assets (Capital Gains) are taxed differently:

-

Individuals: Taxed at a rate of 10% (Source 1.1).

-

Companies: Taxed at a rate of 30% (Source 1.1).

-

Planning: Expats must coordinate the timing of asset sales (e.g., selling Sri Lankan real estate or CSE shares) with their tax residency status to optimize the Capital Gains Tax liability.

-

2. Seeking Specialized Tax Advisory

Navigating multi-jurisdictional tax law (e.g., the UK’s non-dom status vs. Sri Lanka’s residency test) is highly specialized.

-

Affiliate Opportunity: The diaspora needs access to advisors who specialize in global taxation for Sri Lankans. This presents a high-value affiliate opportunity (DoFollow Link: Expat Tax Advisory Service). Seek partnerships with global firms that have a presence in Colombo and major diaspora hubs (Source 3.1).

3. Utilizing Tax-Exempt Investments

Certain local investments and benefits remain tax-exempt (Source 1.1):

-

Any amount received from an approved Provident Fund.

-

Pension or retiring benefits paid by the Government.

Conclusion

The new tax guide for sri lankan expats confirms that passive compliance is no longer enough. The 2026 fiscal regime is clear: all foreign-sourced income, if remitted via the banking system, must be accounted for under the new 15% final tax rule. For the global Lankan, proactive tax planning, stringent adherence to the 183-day residency rule, and the strategic application of DTAAs and FTCs are the only ways to legally protect wealth, maximize returns from Sri Lankan investments, and remain compliant in both their host country and the Motherland. The investment in professional tax advice is now a mandatory part of every expat’s financial portfolio.

Here are two distinct image prompts for this article:

Image Prompt 1: Residency and the Global Asset Map

A highly professional, stylized image. The foreground shows a close-up of a passport and a bank statement/remittance slip (representing the 183-day rule and remittance). In the background, a faint but detailed world map is overlaid with interconnecting red lines (DTAA routes) and a magnified circle focusing on Sri Lanka. A prominent “15%” figure is displayed over the remittance slip. The image conveys complexity, global movement, and the focus on the new tax rate.

Image Prompt 2: Tax Planning Strategy

A clean, modern flat-lay image showing various tax documents from two different countries (different currencies visible), a calculator, and a pair of hands using a smartphone app to check exchange rates (representing Wise or a similar money transfer service). The overall message is financial control and strategic planning.

This video discusses the 2026 Budget, which introduces the significant tax changes impacting foreign income earners and residents, directly providing context for the new tax landscape discussed in the article.

Hidden Tax Increases in the Budget 2026 – Explained! – Taxadvisor.lk

news via inbox

Nulla turp dis cursus. Integer liberos euismod pretium faucibua

Great article on tax residency and remittance rules for Sri Lankan expats! One question that came to mind while reading: How does obtaining a foreign tax identification number (like Spain’s NIE for digital nomads) impact tax residency status under Sri Lanka’s 183-day rule? I recently used https://e-residency.com to get my NIE remotely, but I’m unsure if holding this affects my Sri Lankan tax obligations. Does anyone have experience with dual residency scenarios involving official foreign IDs? Would appreciate any insights!